View Section Menu

NAHB Spring 2026 Economic Update

Category: Build-Remodel-Topics, Industry-Statistics06/23/2026

NAHB economist outlines market outlook for this year

At the National Association of Home Builders Spring Leadership Conference in early June, Chief Economist Dr. Rob Dietz shared a comprehensive look at where the U.S. economy is currently, where it’s headed and what it means for housing and construction. To watch his presentation, click here (login required).

Here’s a breakdown.

The economy is slowing

The economy is entering a slower growth phase:

-

Economic growth is trending toward roughly 2%, below the historical average of about 3.4%

- The risk of a recession is elevated (around 40%), but we are not currently in one

- The labor market is cooling slightly, signaling a mild slowdown

Demographics

A major long-term issue is population and workforce growth:

- Population growth is slowing significantly

- Fewer births are leading to weaker “natural” population growth. Births are not keeping up with deaths.

- The industry is becoming increasingly reliant on immigration for workforce supply

Why it matters:

Fewer workers mean tighter labor markets and higher wages. Labor shortages aren’t going away.

Building Industry Association of the RRV CEO Bryce Johnson highlights the importance of local Association efforts, “Your Association and BIA Foundation are actively working to grow the future workforce right here in the Red River Valley. Through programs like the Herdina Construction Trades Camp, partnerships with the Cass County Career Innovation Center and Moorhead Career Academy, and events like the Health, Tech & Trades Career Expo, we are investing in local youth to help ensure our market remains competitive and healthy. This benefits all our members, builders and associates, by keeping productivity strong.”

Artificial intelligence & productivity

Productivity, especially driven by AI, could shape what comes next. The question is, is it leading to higher productivity in the construction sector?

- Higher productivity means stronger growth, lower inflation and better wages

- Lower productivity and a shrinking workforce means higher costs and pressure on interest rates

We’re already seeing real impacts:

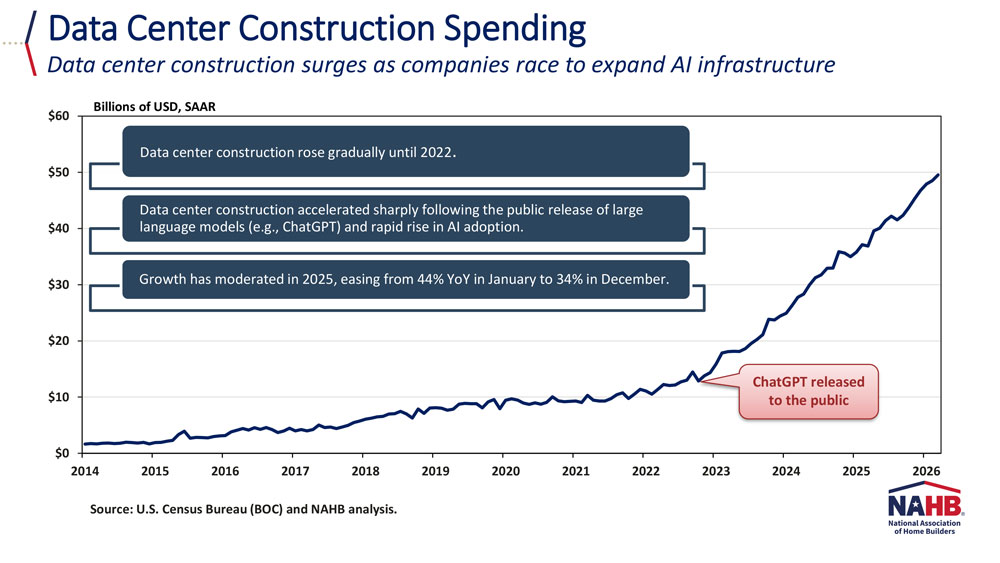

- A surge in data center construction (including activity in North Dakota)

- Increased capital investment tied to AI growth since 2022 (post COVID)

While AI can be a valuable tool for construction companies, it’s important to note a secondary effect: many workers are being drawn to large-scale AI infrastructure projects. This shift is contributing to increased competition for labor and driving up wages, particularly for residential construction.

Wages vs. productivity: still out of sync since COVID

-

Wages have increased faster than productivity

- Productivity dropped sharply, then began recovering

Why this matters:

Long-term wage growth can’t continue unless productivity improves. Otherwise, costs rise and margins diminish.

Why inflation is still a problem

Dr. Dietz highlighted several key drivers behind ongoing inflation:

- Tariffs are increasing the cost of materials and goods

- Immigration policy changes are impacting labor supply and slowing production

- A focus on exports over domestic supply reduces available goods at home

- Global conflicts (Iran war) are pushing up energy costs

- Diesel prices are up 60%

- Policy uncertainty is making businesses hesitant to invest

- Lower bond market activity

- Delayed projects due to lack of confidence

Johnson notes that, “Uncertainty is slowing down projects and disrupting planning for our Builder members. We’ve seen a slowdown in building permit activity locally over the past year and into the start of this year. Consumers and builders are being cautious, and all of this also impacts our Associate members, especially trade partners who work directly on projects, those that fund projects, or those that supply materials.”

Housing & construction market snapshot

Interest rates & costs

-

Mortgage rates remain above 6%, but are gradually trending downward

-

Building material costs are up about 6-7% (as of May)

-

Key materials:

- Copper: up ~35% (~$6/lb)

- Aluminum: rising

Johnson adds, “While mortgage rates remain around 6%, that’s still a historically strong rate. In the Red River Valley, we also have lenders offering a variety of programs to help with the cost of homeownership. We always remind folks: marry the home, date the rate.”

Labor trends

-

Construction workforce is shifting:

-

“White collar” roles in the trades increased from 29% in 2005 to 41% in 2024

- This reflects two likely reasons:

- More technology use

- Growing regulatory complexity

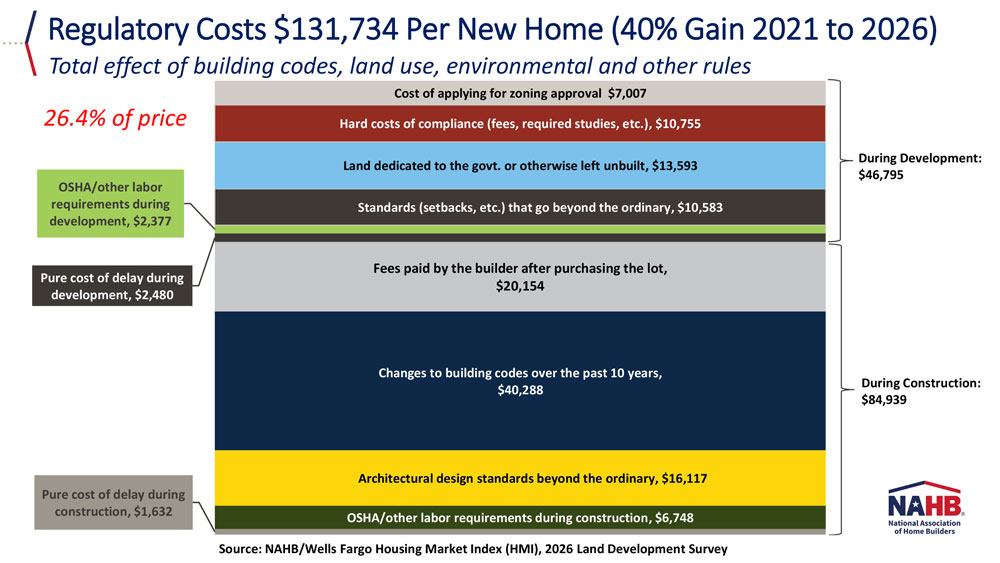

The biggest cost driver: regulation

The most impactful takeaway: Regulatory costs now average $131,734 per new home. That’s a 40% increase since 2021 and represents 26.4% of the total home price

These costs include:

- Building codes

- Land-use regulations

- Environmental requirements

- Permitting and compliance

- And more.

This is one of the biggest obstacles to affordability.

Housing activity trends

- Midwest new home sales: up 6%

- National new home sales: down 6-7%

- Custom home building: increasing

- Housing starts: declining, especially in spec building

- Spec building is pulling back due to uncertainty and cost pressures

Remodeling market outlook: a bright spot

There’s good news: the residential remodeling sector is expected to see continued growth

Why?

- Homeowners are staying put longer

- High interest rates discourage moving

- Demand for upgrades and improvements remains strong

Key takeaways for the industry

- Expect a slower, but stable, economy

- Labor shortages and demographic challenges are here to stay for now

- AI and productivity gains could be the difference-maker

- Regulations are a major cost driver, and continue to rise

- Uncertainty is the biggest near-term risk to growth

Written by Elizabeth Kosel, Education & Public Affairs Specialist